How the Pre-2020 Restricted Application Actually Worked for Widows

A widow restricted application social security strategy is a pre-2020 claiming method that allowed a widow to file for survivor benefits at full retirement age while letting her own retirement benefit grow until age 70. This option is available only if you were born before January 2, 1954. Understanding the filing deadlines and earnings test rules is critical for maximizing your household income.

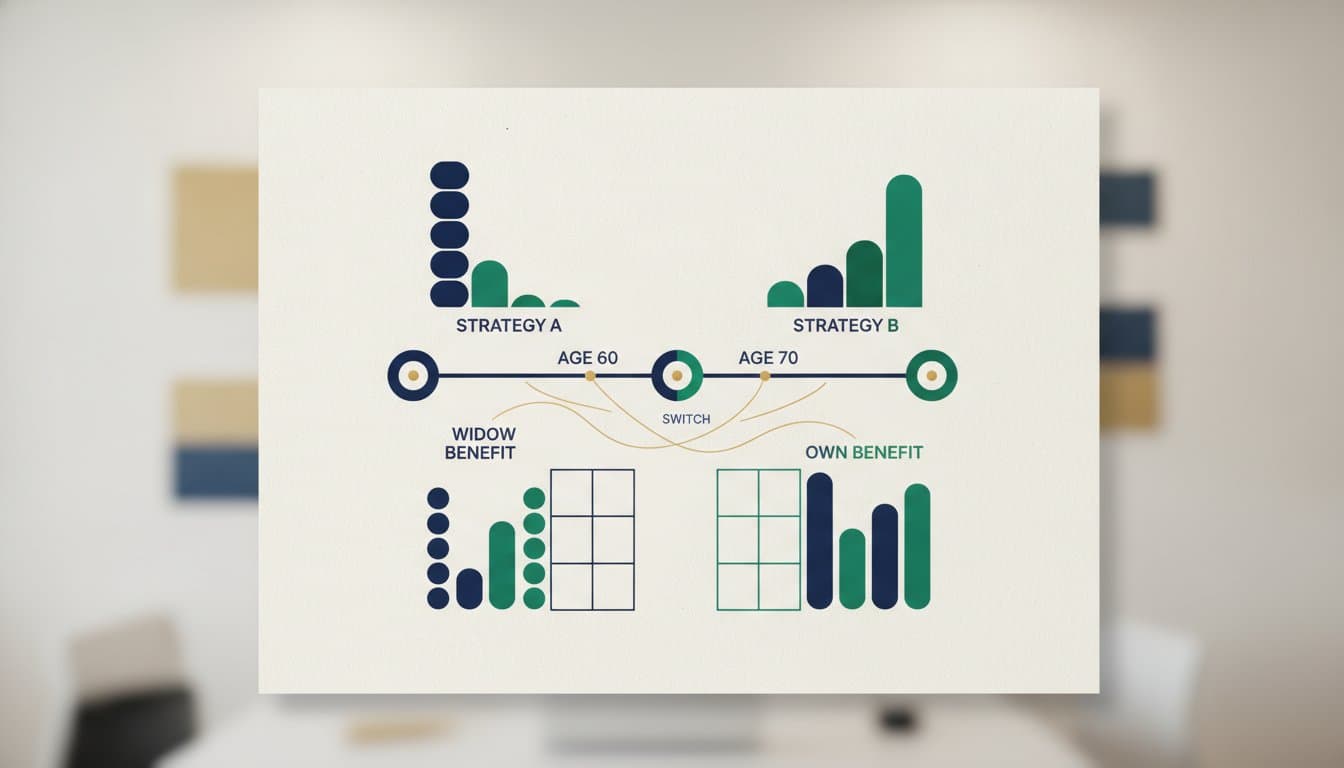

The restricted application was a filing option that let a widow claim only the survivor benefit from her deceased spouse's record without being deemed to file for her own retirement benefit. This was critical because Social Security's "deemed filing" rule normally forces a person who files for one benefit to file for all benefits they are entitled to receive. The Bipartisan Budget Act of 2015 eliminated deemed filing exceptions for spousal benefits, but the survivor benefit restricted application remained available for widows who reached age 62 before January 1, 2020.1

Consider a widow born in 1955 who turned 62 in 2017. Under the pre-2020 rules, she could file a restricted application for survivor benefits at her Full Retirement Age and receive her deceased husband's full benefit — for example, approximately $1,800 per month — while her own retirement benefit of roughly $1,200 per month earned delayed credits at 8% per year.2 By age 70, her own benefit would grow to about $1,584 per month, a 32% increase.2

The strategy worked because survivor benefits do not earn delayed credits after Full Retirement Age. A widow who waits until age 70 to claim survivor benefits receives no increase beyond the FRA amount. By claiming the survivor benefit early and delaying her own benefit, she maximized both income streams.

Who Still Qualifies for a Restricted Application After 2020

The restricted application for survivor benefits remains available only to widows who turned 62 before January 1, 2020. This means widows born before January 1, 1958, are the last cohort eligible to use this strategy. For widows born in 1958 or later, the restricted application is no longer an option — they must file for whichever benefit is higher and accept the deemed filing consequences.3

The eligibility window is narrow. A widow born in 1957 turned 62 in 2019, giving her one year to qualify before the 2020 deadline. A widow born in 1954 turned 62 in 2016 and had four years of eligibility. The table below shows the cutoff:

| Birth Year | Turned 62 | Restricted Application Eligible? |

|---|---|---|

| 1953 or earlier | 2015 or earlier | Yes |

| 1954 | 2016 | Yes |

| 1955 | 2017 | Yes |

| 1956 | 2018 | Yes |

| 1957 | 2019 | Yes |

| 1958 or later | 2020 or later | No |

Widows who are already receiving survivor benefits but have not yet claimed their own retirement benefit may still switch if they meet the age and timing requirements. The Social Security Administration allows one switch between survivor and retirement benefits between Full Retirement Age and age 70.4

Calculating Your Break-Even: Survivor Benefit vs. Your Own Delayed Credits

The decision to use a restricted application hinges on comparing two income streams: the survivor benefit claimed now versus the delayed retirement credits on your own benefit. Suppose a widow's survivor benefit at Full Retirement Age is $2,000 per month, and her own benefit at FRA is $1,400 per month. If she claims the survivor benefit at 66 and delays her own benefit to 70, her own benefit grows to $1,848 per month — an additional $448 per month for life.5

The break-even analysis compares the total dollars received under each strategy. If she claims her own benefit at 66 instead, she receives $1,400 per month for four years ($67,200) but loses the $448 monthly increase for the rest of her life.5 The break-even point occurs around age 82 — if she lives past 82, the delayed claiming strategy produces more lifetime income.

| Claiming Strategy | Monthly Income at 66 | Monthly Income at 70 | Total by Age 82 |

|---|---|---|---|

| Claim own benefit at 66, survivor at 70 | $1,400 | $3,400 | $326,400 |

| Claim survivor at 66, own benefit at 70 | $2,000 | $3,848 | $350,976 |

The second strategy yields approximately $24,576 more by age 821. For widows with longer life expectancies, the gap widens significantly.

The SSA Filing Process Widows Must Follow (No Online Option)

Survivor benefits cannot be applied for online. Widows must call the Social Security Administration at 1-800-772-1213 or visit a local Social Security office in person to file a restricted application for survivor benefits.6 This is a critical detail — many widows attempt to file online and receive no response, losing months of potential benefits.

When calling, the widow should explicitly state she wants to file a "restricted application for widow's benefits only." The SSA representative may not be familiar with this pre-2020 strategy, so she should be prepared to reference the Bipartisan Budget Act of 2015 and her birth year. If the representative says the restricted application is no longer available, she should ask to speak with a claims specialist or request a written determination.

The filing requires the deceased spouse's Social Security number, marriage certificate, and death certificate. The SSA may also request the widow's birth certificate and W-2 forms from the past year. Processing typically takes 4-8 weeks, and benefits are paid retroactively up to six months from the filing date.

How Filing Status Changes Affect Your Benefit Election

A widow's filing status changes when she remarries before age 60. If she remarries before 60, she loses eligibility for survivor benefits based on her deceased spouse's record. If she remarries at age 60 or later, she can still collect survivor benefits from her deceased spouse.7

Divorce also affects the strategy. A divorced widow who was married to the deceased for at least 10 years can claim survivor benefits on her ex-spouse's record. The same restricted application rules apply — if she turned 62 before 2020, she can file a restricted application for survivor benefits while delaying her own benefit.

The SSA automatically adjusts benefit amounts when filing status changes. For example, if a widow receiving survivor benefits remarries at 62, her survivor benefit stops. She can then claim her own retirement benefit or, if her new spouse dies, survivor benefits from the new spouse. Each change requires a new filing and may trigger a recalculation of benefit amounts.

Common Mistakes Widows Make When Claiming Survivor Benefits

The most common mistake is assuming the restricted application is completely dead. Many widows born before 1958 are told by friends or even SSA representatives that the strategy no longer exists. They file for their own benefit at 62, locking in a permanently reduced amount, when they could have filed a restricted application for survivor benefits and earned delayed credits on their own record.

Another frequent error is filing for survivor benefits too early without understanding the reduction. For example, survivor benefits claimed at age 60 are reduced by 28.5% compared to the Full Retirement Age amount. A widow who files at 60 receives only 71.5% of the benefit she would receive at 66.8 If she can wait until FRA, she receives 100%.

A third mistake is failing to switch benefits at the optimal time. Some widows claim survivor benefits at 66 and then forget to switch to their own benefit at 70. The SSA does not automatically switch benefits — the widow must file a new application to begin receiving her own retirement benefit with delayed credits.

What to Do If You Already Missed Your Restricted Application Deadline

If a widow already filed for her own benefit before age 70 and missed the restricted application window, she has limited options. Within 12 months of filing, she can withdraw her application by repaying all benefits received. This restores her to the position of never having filed, allowing her to file a restricted application for survivor benefits instead.9

After 12 months, withdrawal is no longer possible. However, the widow can still maximize her survivor benefit by ensuring she claims it at the right time. If her survivor benefit is higher than her own benefit, she should file for survivor benefits as soon as possible. If her own benefit is higher, she should continue delaying her own benefit until age 70.

For widows who missed the restricted application entirely, the best strategy is to compare both benefits at Full Retirement Age and claim the higher one. The survivor benefit may still be larger than her own benefit, especially if the deceased spouse had a higher lifetime earnings record.

Your Next Step

Call the Social Security Administration at 1-800-772-1213 and request a benefit verification letter showing your own retirement benefit amount and your survivor benefit amount based on your deceased spouse's record. Ask specifically whether you qualify for a restricted application based on your birth year. If you turned 62 before January 1, 2020, schedule an appointment at your local SSA office to file the restricted application for survivor benefits only. Bring your marriage certificate, death certificate, and birth certificate to the appointment.